Table of Contents

Expert Insight for the Modern Patriarch

Expert Insight for the Modern Patriarch

The Core Dilemma: Temporary Protection vs. Lifelong Security

At its heart, the choice between Term and Permanent life insurance boils down to a fundamental question: Do you need coverage for a specific period, or for the entirety of your life? The stakes are incredibly high; according to a 2024 LIMRA study, a staggering 4 in 10 households would face immediate financial hardship if a primary wage earner died. Both options serve vital purposes, but their structures, benefits, and costs differ significantly. Understanding these distinctions is paramount to ensuring your policy aligns with your long-term financial goals.

Term Life Insurance: The Strategic Solution for Defined Needs

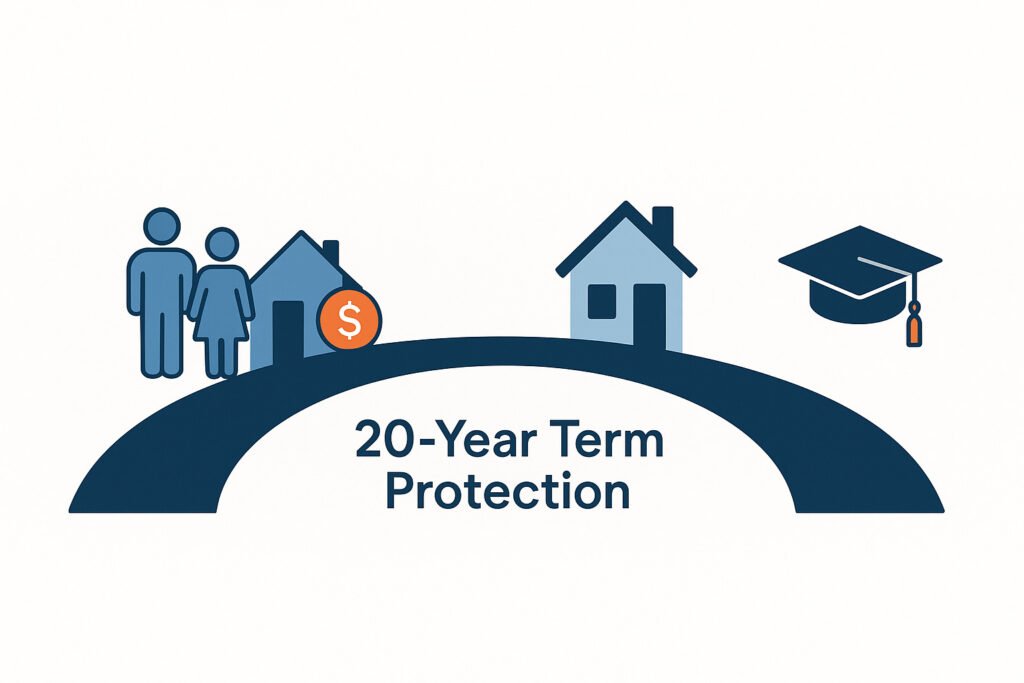

Term life insurance is straightforward: it provides coverage for a specific period, or ‘term,’ typically 10, 20, or 30 years. If you pass away within that term, your beneficiaries receive a predetermined death benefit. If you outlive the term, the policy expires, and there’s no payout. Think of it as renting protection for a set duration.

Why Consider Term Life at 40+?

For men in their 40s, 50s, 60s, and even 70s, term life can be an incredibly efficient tool for specific financial obligations or transitional periods. Consider these scenarios:

For men in their 40s, 50s, 60s, and even 70s, term life can be an incredibly efficient tool for specific financial obligations or transitional periods. Consider these scenarios:

• Mortgage Protection: If you have 10-15 years left on your mortgage, a term policy can ensure your family retains their home free and clear should something happen to you.

• Income Replacement During Working Years: If you’re still actively working and your income is crucial for your family’s lifestyle, a term policy can replace that income until retirement or until your children are financially independent.

• Debt Coverage: Outstanding business loans, personal debts, or even significant car loans can be covered by a term policy, preventing your family from inheriting financial burdens.

• Bridging the Gap to Retirement: A term policy can provide essential coverage until your retirement savings and other assets are robust enough to self-insure.

• Mortgage Protection: If you have 10-15 years left on your mortgage, a term policy can ensure your family retains their home free and clear should something happen to you.

• Income Replacement During Working Years: If you’re still actively working and your income is crucial for your family’s lifestyle, a term policy can replace that income until retirement or until your children are financially independent.

• Debt Coverage: Outstanding business loans, personal debts, or even significant car loans can be covered by a term policy, preventing your family from inheriting financial burdens.

• Bridging the Gap to Retirement: A term policy can provide essential coverage until your retirement savings and other assets are robust enough to self-insure.

The Advantages of Term Life

• Affordability: Generally, term life insurance is significantly less expensive than permanent life insurance for the same amount of coverage, especially in your 50s. This allows you to secure a larger death benefit for a lower premium. [2]

• Simplicity: Its straightforward nature makes it easy to understand and manage.

• Expiration Risk: The most significant drawback is the risk of outliving your policy. If the term ends and you still need coverage, you’ll have to purchase a new policy, which will be considerably more expensive due to your increased age and potential health changes.

• No Cash Value: Unlike permanent policies, term life does not build cash value. It’s pure protection, with no savings or investment component.

• Flexibility: You can choose a term that precisely matches your specific financial needs, and many policies offer convertibility options to permanent coverage later.

The Drawbacks to Acknowledge

While attractive, term life isn’t without its limitations, particularly as you age:

• Expiration Risk: The most significant drawback is the risk of outliving your policy. If the term ends and you still need coverage, you’ll have to purchase a new policy, which will be considerably more expensive due to your increased age and potential health changes. [3]

• No Cash Value: Unlike permanent policies, term life does not build cash value. It’s pure protection, with no savings or investment component.

For men looking beyond immediate needs, permanent life insurance offers unique advantages for long-term financial planning.

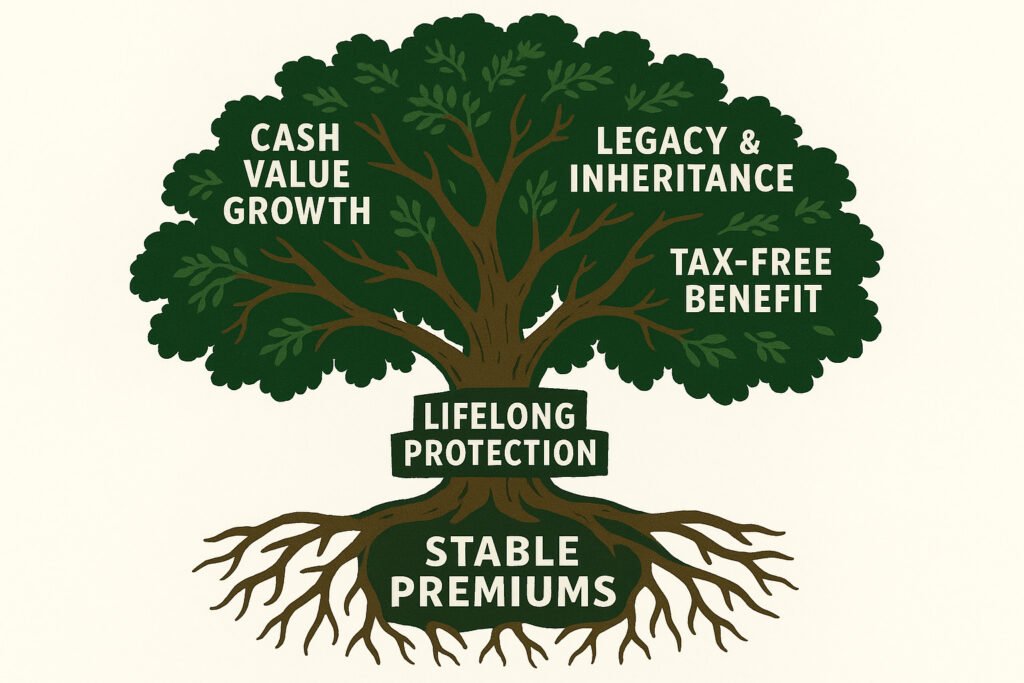

• Guaranteed Lifelong Coverage: The primary appeal is the assurance that your coverage will never expire, providing peace of mind that your beneficiaries will receive the death benefit regardless of when you pass.

• Cash Value Growth: A portion of your premium goes into a cash value component that grows on a tax-deferred basis.

• Estate Planning and Wealth Transfer: Permanent policies are powerful tools for minimizing estate taxes and ensuring specific beneficiaries receive a guaranteed inheritance.

• Business Succession Planning: For business owners, permanent life insurance can fund buy-sell agreements, ensuring a smooth transition of ownership upon your passing or retirement.

• Increasing Costs at Renewal: If you renew a term policy after its initial period, the premiums will likely increase dramatically, reflecting your older age and higher mortality risk. [4]

References: [1] NerdWallet: Term Life vs. Whole Life Insurance: Key Differences and How To Choose. https://www.nerdwallet.com/article/insurance/term-vs-whole-life-insurance [2] Guardian Life: What is the Best Life Insurance for People over 50 Years Old? https://www.guardianlife.com/life-insurance/over-50 [3] Funeral Advantage: Guide to Life Insurance for Seniors Over 60. https://funeraladvantage.com/consumer-resources/life-insurance-for-seniors-over-60/ [4] Guardian Life: The Advantages and Disadvantages of Life Insurance. https://www.guardianlife.com/life-insurance/advantages-and-disadvantages

Permanent Life Insurance: Building a Lifelong Financial Anchor

Permanent life insurance provides coverage for your entire life, as long as premiums are paid. Beyond the guaranteed death benefit, these policies also accumulate cash value over time, which can be accessed during your lifetime.

Why Consider Permanent Life at 40+?

For men looking beyond immediate needs, permanent life insurance offers unique advantages for long-term financial planning, wealth transfer, and legacy building:

• Guaranteed Lifelong Coverage: The primary appeal is the assurance that your coverage will never expire, providing peace of mind that your beneficiaries will receive the death benefit regardless of when you pass. This is particularly valuable for estate planning and leaving a lasting legacy. [6]

• Higher Cost: Premiums for permanent life insurance are significantly higher than for term life, especially when purchased later in life.

• Complexity: These policies can be more complex to understand, with various types, each having different features and risks.

• Long-Term Commitment: It requires a long-term commitment to premium payments to realize the full benefits of cash value growth and lifelong coverage.

• Cash Value Growth: A portion of your premium goes into a cash value component that grows on a tax-deferred basis. This cash value can be accessed through loans or withdrawals, providing a flexible source of funds for emergencies, retirement income, or other financial needs. [7]

• Estate Planning and Wealth Transfer: Permanent policies are powerful tools for minimizing estate taxes, funding trusts, or ensuring specific beneficiaries receive a guaranteed inheritance. The death benefit is typically paid out tax-free to beneficiaries. [8]

• Business Succession Planning: For business owners, permanent life insurance can fund buy-sell agreements, ensuring a smooth transition of ownership upon your passing or retirement.

The Advantages of Permanent Life

• Lifelong Protection: Eliminates the risk of outliving your coverage.

• Increasing Costs at Renewal: If you renew a term policy after its initial period, the premiums will likely increase dramatically, reflecting your older age and higher mortality risk.

• Cash Value Accumulation: Provides a living benefit that can be accessed during your lifetime.

• Temporary Needs: If your primary goal is to cover specific, time-bound financial obligations like a mortgage, raising children, or significant debts, Term life insurance is often the most cost-effective solution.

• Lifelong Needs & Legacy: If you envision leaving a guaranteed inheritance, covering final expenses, or using life insurance as a long-term wealth accumulation tool, Permanent life insurance aligns better with these objectives.

• Tax Advantages: Tax-deferred cash value growth and typically tax-free death benefits.

• Affordability Now: Term life offers a higher death benefit for a lower premium, making it accessible for those who need significant coverage but have budget constraints.

• Long-Term Commitment: Permanent life insurance requires a greater financial commitment upfront, but the premiums are typically fixed for life, providing predictability.

• Stable Premiums: Premiums are often fixed for life, providing predictability in your financial planning.

• Current Health: Your current health status will significantly impact the premiums for both types of policies. The younger and healthier you are, the more favorable your rates will be.

• Future Insurability: If you anticipate future health issues, securing a permanent policy now can guarantee insurability regardless of your health down the line.

The Considerations and Trade-offs

• Estate Taxes: For high-net-worth individuals, permanent life insurance can be a crucial tool for mitigating estate taxes and ensuring your assets are passed down efficiently.

• Charitable Giving: Permanent policies can be used to fund charitable bequests, leaving a lasting impact on causes you care about.

• Equalizing Inheritances: If you have non-liquid assets, a permanent life policy can provide liquid assets to other heirs, ensuring fairness.

While robust, permanent life insurance comes with its own set of considerations:

While robust, permanent life insurance comes with its own set of considerations:

• Complexity: These policies can be more complex to understand, with various types (Whole Life, Universal Life, Variable Universal Life) each having different features and risks.

• Long-Term Commitment: It requires a long-term commitment to premium payments to realize the full benefits of cash value growth and lifelong coverage.

References: [5] NerdWallet: Term Life vs. Whole Life Insurance: Key Differences and How To Choose. https://www.nerdwallet.com/article/insurance/term-vs-whole-life-insurance [6] The American College: The Ultimate Guide for Choosing the Best Type of Life Insurance Policy. https://www.theamericancollege.edu/knowledge-hub/insights/the-ultimate-guide-for-choosing-the-best-type-of-life-insurance-policy [7] Thrivent: Whole life insurance for seniors: 4 reasons to consider it. https://www.thrivent.com/insights/life-insurance/whole-life-insurance-for-seniors-4-reasons-to-consider-it [8] Mutual of Omaha: Life Insurance Over 65: Secure Your Legacy. https://www.mutualofomaha.com/advice/life-insurance/understanding-life-insurance/what-to-look-for-in-life-insurance-over-65 [9] Mutual of Omaha: Life Insurance for People Over 50. https://www.mutualofomaha.com/advice/life-insurance/understanding-life-insurance/life-insurance-for-people-over-50

Term vs. Permanent: A Side-by-Side Comparison for the Discerning Man

Your life’s work, your family’s security, your legacy – these are not things to leave to chance. The decision between Term and Permanent life insurance is pivotal, and it deserves clarity and expert guidance.

term vs permanent life insurance for men

During this brief conversation, you’ll discuss your unique situation and identify the optimal path forward to ensure your family is protected, no matter what the future holds. This isn’t a sales pitch; it’s an opportunity to gain peace of mind and solidify your financial future.

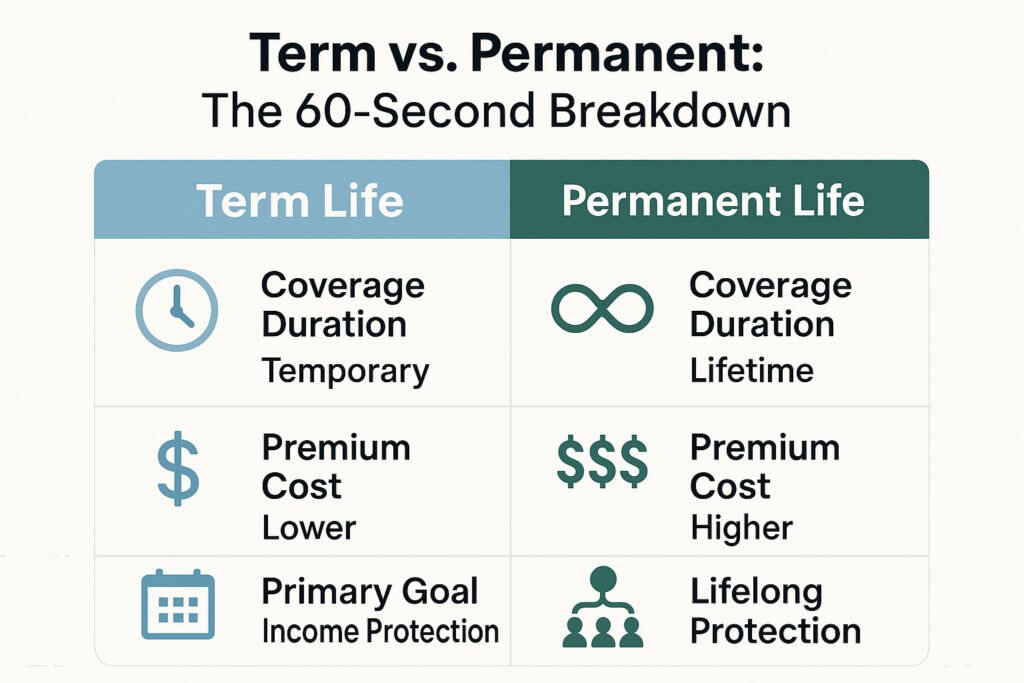

To help you visualize the core differences and make an informed decision, here’s a direct comparison of Term and Permanent life insurance:

| Feature | Term Life Insurance | Permanent Life Insurance |

| Coverage Duration | Specific period (e.g., 10, 20, 30 years) | Entire lifetime |

| Cash Value | No cash value accumulation | Accumulates cash value over time |

| Premium Cost | Generally lower for the same death benefit | Generally higher for the same death benefit |

| Purpose | Income replacement, debt coverage, temporary needs | Lifelong protection, estate planning, wealth transfer |

| Flexibility | Can be converted to permanent (often) | Access to cash value via loans/withdrawals |

| Expiration | Expires at end of term; no payout if outlived | Never expires (as long as premiums are paid) |

| Complexity | Simple and straightforward | More complex, with various types (Whole, Universal, etc.) |

| Tax Benefits | Death benefit typically tax-free | Tax-deferred cash value growth; death benefit tax-free |

Making Your Choice: A Strategic Framework

The decision between Term and Permanent life insurance is deeply personal and depends on your unique financial situation, goals, and priorities. Consider the following:

1. Define Your “Why”: What Are You Protecting?

• Temporary Needs: If your primary goal is to cover specific, time-bound financial obligations like a mortgage, raising children, or significant debts, Term life insurance is often the most cost-effective solution. It provides substantial coverage during the years your family is most financially dependent on your income.

• Lifelong Needs & Legacy: If you envision leaving a guaranteed inheritance, covering final expenses, funding a trust, or using life insurance as a long-term wealth accumulation tool, Permanent life insurance aligns better with these objectives. It ensures a death benefit will be paid regardless of when you pass, and the cash value can serve as a valuable asset during your lifetime.

2. Assess Your Budget and Financial Capacity

• Affordability Now: Term life offers a higher death benefit for a lower premium, making it accessible for those who need significant coverage but have budget constraints. It allows you to maximize protection during your peak earning years.

• Long-Term Commitment: Permanent life insurance requires a greater financial commitment upfront, but the premiums are typically fixed for life, providing predictability. Consider if you are comfortable with the higher ongoing cost for the lifelong benefits and cash value growth.

3. Consider Your Health and Age

• Current Health: Your current health status will significantly impact the premiums for both types of policies. The younger and healthier you are, the more favorable your rates will be. This is particularly true for permanent policies, where the fixed premium locks in your rate for life.

• Future Insurability: If you anticipate future health issues, securing a permanent policy now can guarantee insurability regardless of your health down the line. Term policies, upon renewal or conversion, will reassess your health.

4. Evaluate Your Estate and Legacy Goals

• Estate Taxes: For high-net-worth individuals, permanent life insurance can be a crucial tool for mitigating estate taxes and ensuring your assets are passed down efficiently.

• Charitable Giving: Permanent policies can be used to fund charitable bequests, leaving a lasting impact on causes you care about.

• Equalizing Inheritances: If you have non-liquid assets (like a family business) that you wish to pass to one heir, a permanent life policy can provide liquid assets to other heirs, ensuring fairness.

Your Action Plan: Moving from Choice to Certainty

Making the right life insurance decision is a significant step in securing your legacy. It’s not about picking one over the other blindly, but rather understanding which type best serves your unique objectives.

- Revisit Your Financial Blueprint: Take stock of your current assets, liabilities, income streams, and future financial obligations. What specific needs do you want life insurance to address? Is it debt coverage, income replacement, estate planning, or a combination?

- Project Your Future Needs: Consider your long-term goals. Do you anticipate needing coverage for your entire life, or only for a defined period? What kind of legacy do you wish to leave?

- Consult an Expert: This is where my 15 years of experience as a CFP® becomes invaluable. While this guide provides a comprehensive overview, your individual circumstances require personalized analysis. A brief, focused conversation can clarify complexities, address your specific concerns, and help you tailor a strategy that perfectly fits your needs.

Protect What You’ve Built: Schedule A Call With Your Agent

Your life’s work, your family’s security, your legacy – these are not things to leave to chance. The decision between Term and Permanent life insurance is a pivotal one, and it deserves the clarity and expert guidance that only a seasoned professional can provide. Don’t navigate these waters alone.

During this brief conversation, you’ll discuss your unique situation, clarify any lingering questions, and identify the optimal path forward to ensure your family is protected, no matter what the future holds. This shouldn’t a sales pitch; it’s an opportunity to gain peace of mind and solidify your financial future.